On-ramps and Off-ramps: Fintech x DeFi Crossover

Transforming money and moving quickly

Welcome to another edition of the DeFi Mullet newsletter! In this newsletter, I hope to cover the arguably boring world of the most anticipated collab of the decade: Fintech x DeFi (ft. policy, markets, tech, product, etc).

If you are one of the fine folks who get a thrill from these topics, press subscribe below!

In the world of DeFi, there are a variety of truly hard problems of which there are many people meaningfully trying to make a difference. One such problem that has substantial overlap with traditional finance is the need for seamless on-ramps and off-ramps.

An on-ramp is a mechanism that enables a user to exchange their fiat for tokens, with the destination being the user’s DeFi wallet (non-custodial)

An off-ramp is a mechanism that enables a user to exchange their tokens for fiat, with the destination being the user’s bank account (custodial)

For the sake of sanity, we will simply refer to on-ramps and off-ramps in the collective as ramps.

Although it may sound like a simple problem there is boundless complexity that comes when operating at the intersection of the old world and the new. The upside of getting this right is undoubtedly massive but the journey of getting there will require the successful navigation of great ambiguity. In a hot market, it can be difficult to distinguish signal from noise, especially amongst rocketing valuations, VCs clamouring for allocations, and founders promising the world. It is appropriate that we reflect on what we are building, why we are building it, and the principles that underpin the future we aspire to inhabit.

This post will touch on the following: the composability of ramps; companies leading the way; a broader snapshot of the market; identification of some of the sticky issues; and a view of the future.

It’s a sign of the times: @jenny_colgate and @NikMilanovic

How far we have come

The more crypto native we become the easier it is to forget what it was like staring at crypto for the very first time. For many, the on-ramp process required several days of waiting whilst also navigating centralised exchanges, banks, and manually setting up an Ethereum wallet - the anxiety of not knowing whether your money would be lost was real. Ramps promise to make this experience as frictionless and inexpensive as possible. For crypto to truly reach mass adoption the level of complexity a user is burdened with must trend downwards, to the point where the underlying technology is entirely abstracted away - how many people know how a card payment works? Despite what you may think concerning a fully decentralised future, it is clear that medium-long term development will require a dual-track existence of both regulated traditional fiat and unregulated/lightly regulated crypto. Ramps will form the foundation of the bridge that binds these two worlds together.

The composability of on-ramps and off-ramps

Ramps are a story of composability and several general-purpose fintech developments enable them to scale sustainably.

Building block 1: Card networks (Visa, Mastercard)

Enable interoperability at scale between issuing banks and acquiring banks

Building block 2: Payment gateways (Stripe)

Provide an easy to implement solution for aggregating across card networks to provide customers with multiple options to pay

Building block 3: Instant payment networks (Instant ACH, Faster Payments)

Settle interbank transactions instantly cf. standard ACH clearance of 3-4 business days

Building block 4: Open banking (Plaid)

Provide an easy to implement solution for aggregating the routing that facilitates the account-to-account (A2A) transfers in building block 3

Building block 5: KYC / AML automation (Alloy, Sardine)

Provider an easy to implement solution for aggregating across multiple KYC / AML check types and providers (PEPs / Sanctions, eKYC, and ID&V)

Building block 6: Advanced embeddable fraud detection (Sardine, SEON)

Provide an easy to implement SDK to capture as much secondary user data as possible to inform fraud risk models i.e. device type, user gestures, IP address, etc.

Building block 7: API access to P2P/OTC fiat-to-crypto exchanges (Binance, Gemini, Coinbase, Prime Trust liquidity-as-a-service, ZeroHash liquidity-as-a-service)

Provide access to deep pools of fiat-to-crypto liquidity to enable quick settlement times while also allowing ramps to sustainably scale

Building block 8: On-chain wallet risk screening (Elliptic, Chainalysis, Merkle Science)

Mitigate regulatory and financial crime risk by analysing the risk of destination crypto wallets using on-chain and, where possible, off-chain data

Giddy is partnering with Plaid and Wyre to enable speed

Core business model considerations

The three core considerations of an on-ramp/off-ramp are speed, risk management, and price. Speed and risk management are fundamental drivers of the unit economics (read as: price) that underpin any promising on-ramp/off-ramp company.

Producing fast ramps will lead to a substantial reduction of friction and the widest adoption of DeFi. Users are increasingly accustomed to near-instant payments powered by the development of instant payment rails such as Faster Payments and Instant ACH. It stands to reason that interoperability between fiat and DeFi should not deviate from that standard. It is important to note that true speed has only been made possible given the recent ubiquity of faster settlement times, open banking, KYC automation, and API based access to deep pools of market liquidity.

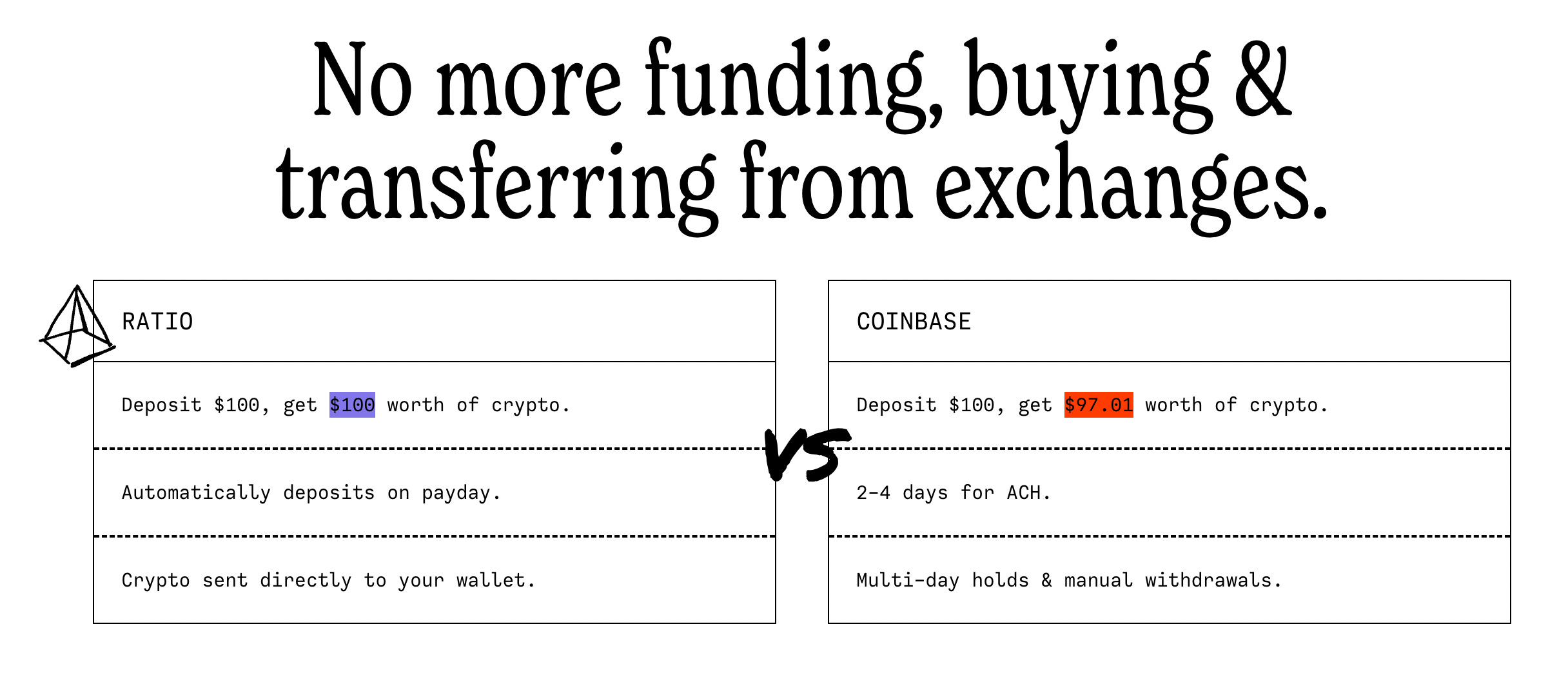

Ratio compares the old and the new

The second core consideration is risk management: regulatory risk (KYC / AML) and financial crime risk (fraud). In traditional financial services, KYC / AML required the manual verification of an individual’s identity often using a combination of physical government identification and third party data such as credit reports or utility bills. Fintech upended this approach by utilising artificial intelligence, biometrics, and simple to use APIs to automate much of this operational overhead. Ramps can simultaneously increase speed and mitigate regulatory risk by integrating best-in-class KYC / AML solutions throughout customer onboarding. Financial crime risk is a harder problem to crack given the limited dataset available to ramps at the point of a transaction. Companies like Sardine and SEON provide ramps easy to integrate SDKs which enable the collection of a wider set of secondary user data to better inform ML-based risk models. Companies like Elliptic and Chainalysis provide expertise in assessing on-chain risk and are crucial service providers for mitigating risk exposure, which is especially important for off-ramping.

The final core consideration of any promising ramp business is price. The price shown to a customer is most often a combination of network fees (read as: gas - layer 2 solutions will continue to push network fees down) and processing fees (charged by the ramp). A ramp’s ability to scale will come down to the unit economics underpinning the structure of the processing fees being levied. At its simplest level, a transaction is:

TradFi costs (e.g. card networks, payment gateways, open banking) +

Costs of risk mitigation (KYC, fraud analytics, on-chain analytics) +

OTC execution costs +

Margin*

= Processing Fees

*As the broader market trends towards commoditisation, major ramps will inevitably suffer margin compression. Much like interchange in retail markets, it would not be shocking if regulatory pressure fixes this cost in the medium term. The ramps that best execute on keeping total transaction costs as low as possible will be best positioned to handle serious on and off-ramp transaction volume.

A ramp’s approach to risk mitigation can also substantially reduce the ongoing operational costs of risk management. One cost worth mentioning is managing disputes and chargebacks as a result of nefarious actors. It is interesting to note that companies like Sardine offer fraud indemnification as a core selling point of their product.

Sardine’s website highlighting fraud indemnification

The early leaders

It is early doors but several leading companies stand out from the rest of the pack. There have been some war chest sized rounds raised as well as a rush to close as many low hanging fruit opportunities for distribution as possible.

Founded: 2019

Last Round: $555m Series A - November 2021

Valuation: $3.4b

Founded: 2018

Last Round: SPAC (NYSE:BKKT) - October 2021

Valuation: ~$780m

Founded: 2019

Last Round: $2.4m Seed - July 2021

Valuation: undisclosed - important to highlight Transak’s whopping growth over the last 12 months; it would not be surprising if Transak are currently looking to raise their Series A

Founded: 2017

Last Round: $30m Series A - October 2021

Valuation: $300m

Founded: 2013

Last Round: Acquired by Bolt - April 2022

Valuation: Sale price of $1.5b

Broader landscape

Numerous companies are emerging and they have been grouped according to their value proposition.

Differentiated Product-Suite (B2B2C)

Differentiated Product-Suite (B2C)

OnJuno - broader banking meets crypto play where ramps are a component (consumer)

Kash - broader banking meets crypto play where ramps are a component (consumer and business).

Speed & Simplicity

Strategic TAM expansion

Ratio - strategically targeting payroll as the core opportunity for broader TAM expansion

Aggregation

OnRamper - in composable technology stacks, aggregation is an inevitability: see Alloy for KYC and 1inch for DEXs,

View for the future

With so many emergent companies the rush for land will no doubt be swift and decisive. The first step is to survive and to survive requires mastery of the fundamentals: speed, risk management, and price. As we have seen time again in the building block thesis of fintech, commoditisation is the inevitability and there is only room for a handful of true return-the-fund size winners. The second step is to understand how to operationalise and execute upon TAM expansion. Companies must have unique insight as to how best meet the user at the very point the reduction of friction is needed. The lowest hanging fruit has already been seized: Moonpay and Opensea, Transak and Metamask, Wyre and Rarible. There are a number of approaches that could be considered as short-term strategic differentiators to fuel initial expansion: access to the widest set of L1s and L2s; simplest to embed on 3rd party websites; geo-specific customisation; best-in-class collaboration with regulators; leveraging adjacencies for distribution (a la Stripe); and early monopolisation of newly identified points of friction.

Ramps, in the short-medium term, will continue to face challenges in four areas:

Managing financial crime risk on both sides, TradFi and DeFi;

Managing regulatory risk and collaborating with regulators;

Continuing to improve interoperability and backward compatibility with TradFi (see Fiat Republic as a provider building fiat plumbing to address this problem) ; and

Handling unhappy paths at scale i.e. chargebacks.

Despite these challenges, ramps have a tremendously promising future. It will not be a winner-takes-all outcome but there will be a handful of dominant players with a long-tail of smaller companies that service a particular niche or excel in a particular aspect of their product offering.

If you are a technical or non-technical and exploring what’s next, would love to chat - please reach out via DM on Twitter 🙏